The global economy is faced with a synchronized slowdown as central bank ammunition to fight the next global recession is limited.

Monetary authorities across the world have slashed interest rates 80 times over the last 12 months and printed upwards of $1 trillion over four months to counter the slowdown.

The only apparent solution central bankers have offered is a liquidity-fueled massive stock market melt-up across the world that rivals the end years of the Dot Com bubble (and the liquidity-fueled meltup around Y2K). These unelected officials have also provided forward guidance on how an epic V-shape recovery in the real economy is imminent.

The only problem today that market watchers like ourselves have noticed – is that traditional monetary policy has had a challenging time stimulating growth in developed and emerging economies.

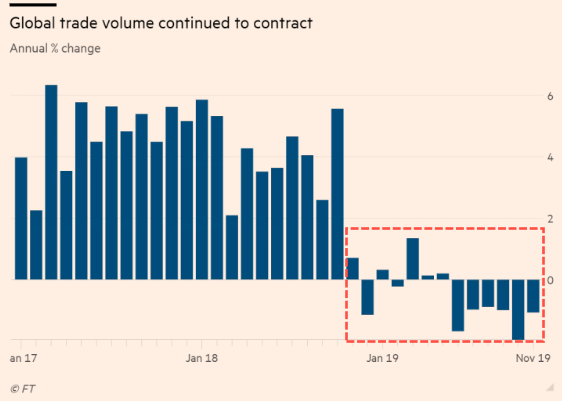

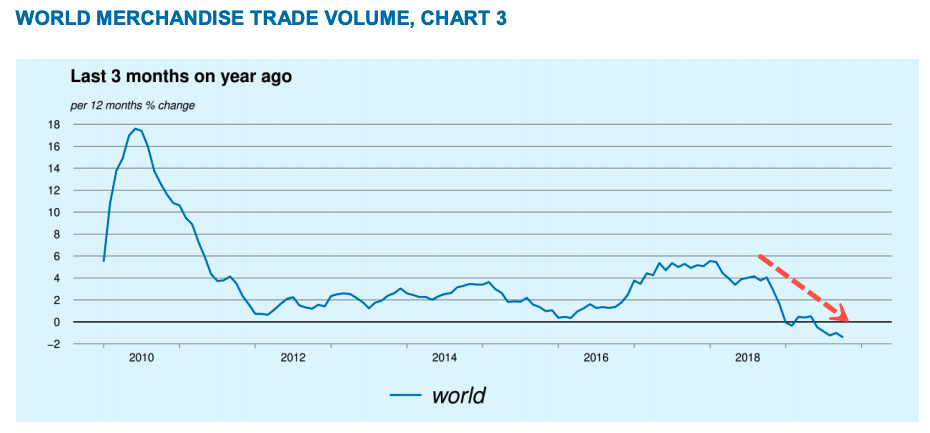

Data from Netherlands Bureau for Economic Policy Analysis (CPB) showed Friday that global trade volume continued to contract in November, marking one of the most extended stretches of negative growth since the end of the financial crisis.

According to CPB, world trade slipped 0.60% in November over the prior quarter and was down 1.1% compared to the same month a year ago.

November was the sixth month of straight of declines on a Y/Y basis, the longest stretch since right after the 2008 financial crisis.

World trade has dropped sharply from 3.4% in November 2018.

However, there was some good news; the rate of contraction has slowed from a -2% pace seen in October, which was the quickest rate of decline since a decade ago.

And while hope is high that the so-called 'trade deal' will lift all boats, data shows that the global economy has continued slowing into 2020 as the Baltic Exchange's main sea freight index has crashed 70% in the last four months, the biggest down moves since 2008.

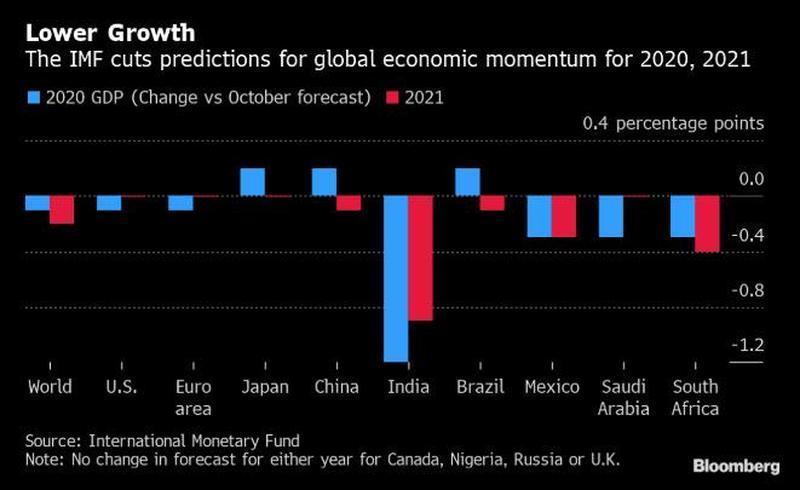

Additionally, earlier this week, the IMF downgraded its forecast for global GDP for 2020 and 2021, its sixth straight reduction, although in a sliver of optimism, global GDP in 2020 is now expected to post a modest rebound from 2.9% to 3.3%, (down from 3.4% in October) and to 3.4% in 2021 (down from 3.6%) as the IMF said, "there are now tentative signs that global growth may be stabilizing, though at subdued levels."

Before Davos this week, the World Economic Forum (WEF) President Borge Brende warned the world is "faced with a synchronized slowdown in the global economy. And we're also faced with a situation where the ammunition that we have to fight a potential global recession is more limited."

Last week, the UN published its annual report that warned the global economy recorded its lowest growth in a decade in 2019, falling to 2.3% as a result of...